what's your SaaS company Worth in 2026?

The formula exists. Most founders just never find it before it's too late.

Someone makes you an offer. A number lands on the table.

And right there, in that moment, you realize you have no idea if it’s good or not.

Most SaaS founders hit this wall. They’ve been heads-down building, and the valuation question always felt like something to figure out later. So they anchor to whatever 2021 horror story they read on Twitter, or they accept the first number that sounds reasonable, with nothing solid to push back with.

What very few people realize is that private SaaS valuations are far more quantifiable than they look. There’s a regression-derived formula, built from 63 real private-market cash transactions, that gives you a defensible baseline multiple before anyone sits across the table. The inputs are three metrics you almost certainly track already.

This is that framework.

Where private SaaS deals are actually pricing in 2026

The 2021 era of 15x-18x ARR multiples is gone, and it’s not coming back. What replaced it is a more disciplined market where the gap between an average exit and a great one has never been wider. Two companies with identical ARR can sell at prices that differ by 3x or 4x, depending on the same handful of variables.

As of Q1 2026, here’s where private B2B SaaS transactions are landing:

Bootstrapped companies with moderate growth are pricing around 4.8x ARR

Equity-backed companies with moderate growth are pricing around 5.3x ARR

Companies with Rule of 40 above 50 and NRR above 120% are closing at 7x to 9x ARR

High-growth outliers running a competitive buyer process are reaching 10x to 12x ARR — though fewer than 5% of private deals get there

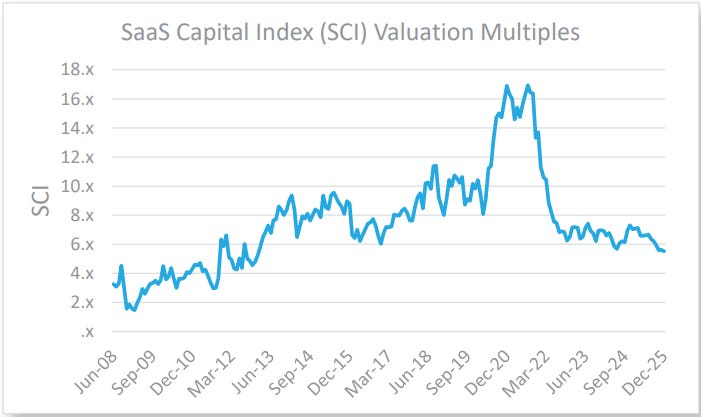

The public SaaS benchmark — the SaaS Capital Index, which tracks 102 curated B2B SaaS companies — sits at 5.5x as of Q1 2026. Private companies transact at a discount to this, but how much of a discount depends almost entirely on three company-specific inputs.

The founders who get the best outcomes aren’t necessarily running the fastest-growing companies. They’re the ones who understood this math early enough to do something about it.

The three inputs behind every private SaaS multiple

Every valuation multiple for a private B2B SaaS company flows from three factors:

1. Broad market conditions Tracked through the SaaS Capital Index — a monthly-updated barometer of what public SaaS companies are trading at. Think of it like price-per-square-foot in real estate: it sets the market temperature before any deal-specific factors come into play.

2. ARR growth rate The single most weighted variable in the formula. Statistically, it has the strongest correlation with observed multiples across 60+ real transactions. And it has to be calculated correctly — annualized, actual, run-rate, not projected. The distinction matters more than most founders expect.

3. Net Revenue Retention (NRR) The quality signal. NRR tells buyers whether your existing customer base is expanding or quietly contracting, and it carries information that growth rate alone doesn’t: pricing power, customer satisfaction, and product stickiness in a single number. Best-in-class companies in the $1M–$10M ARR range consistently land between 100% and 110% NRR.

These three inputs go into a specific formula. The output is a baseline multiple. From there, real deals move up or down based on factors that never appear in any lookup table — and that most founders don’t know to prepare for.

What premium subscribers get

The free section covers the context and the inputs. Everything below the paywall is the actual working framework:

The exact formula with three worked examples at different ARR and growth profiles, so you can run your own number in under five minutes

The full Q1 2026 baseline multiples, covering ARR growth from 10% to 150% across seven NRR bands — your number is in there

How to calculate NRR correctly, including the mistakes that inflate or deflate it before a buyer’s diligence model corrects it for you

The 7 threshold assumptions that determine whether this model applies to your business, and what to do if your metrics fall outside them

Additive adjustments — what gets added or subtracted from the pure SaaS valuation in an actual M&A transaction, including non-SaaS revenue lines, balance sheet items, and earnout structures

The four silent deal-killers that never appear in a formula but routinely reprice deals late in diligence, sometimes by millions

The AI multiple premium — when proprietary AI integration genuinely shifts your valuation, and when buyers read it as a product story with no financial substance

The process gap — why a structured competitive sale consistently adds 1x–2x ARR over a bilateral negotiation, and what that looks like in actual dollar terms on a $5M ARR business

Free 7-day trial. Cancel anytime.

The Full Framework: What Your SaaS Company Is Actually Worth

Let’s start with the most important thing

The baseline valuation multiple for a private B2B SaaS company is not a gut feeling, not a comp pulled from a TechCrunch headline, and not whatever number a banker throws at you in a first call. It’s the output of a specific formula, derived from 63 real private-market cash transactions, and it’s been statistically validated across more than a decade of market cycles.

Here it is.

The Formula:

Keep reading with a 7-day free trial

Subscribe to The VC Corner to keep reading this post and get 7 days of free access to the full post archives.