SpaceX Just Filed the Biggest IPO in History. Here Is What the Numbers Actually Say

$1.75 trillion. $75 billion raise. Three businesses with completely different financial profiles sold as one number. Here is the teardown.

SpaceX wants to go public at $1.75 trillion.

That would be the largest IPO ever recorded, bigger than Ant Financial and Saudi Aramco. The S-1 landed on May 20, with a Nasdaq debut targeted for June 12 under the ticker SPCX and a raise of up to $75 billion.

Lead underwriters: Goldman Sachs, Morgan Stanley, BofA, Citi, and JPMorgan.

For the first time, we can read the actual financials behind the most valuable private company ever built.

Most of the coverage is getting the central point backwards.

Every outlet is quoting $18.7 billion in 2025 revenue. That figure combines three companies. SpaceX merged with xAI in February 2026. xAI had already absorbed X in March 2025. Because these deals happened between entities under common control, the accountants recast every historical period to fold all three together.

Standalone SpaceX did closer to $15 to $16 billion in 2025. The merged entity reports $18.7 billion. The gap is xAI and X, and that gap arrives carrying enormous losses.

You are pricing a cash-generative satellite business stapled to a money-losing AI business and a launch business that reinvests everything. To value SpaceX, you have to take the three apart.

Before we go deeper, the IPO will instantly reprice the entire space sector. Here is where every major name sits heading into June 12:

Satellogic up 407% YTD. Planet Labs up 110%. AST SpaceMobile up 12%. Rocket Lab up 76%. Every one of these companies trades differently the moment SPCX prices.

If you want to understand how to analyze these kinds of opportunities with AI, the stock analyst prompts guide gives you 12 copy-paste prompts for institutional-grade research. And if you want a framework for how to think about the SpaceX strategy and pitch deck before the S-1, we broke that down too.

Three Businesses, Three Completely Different Financial Profiles

The official S-1 connectivity slide tells you the scale before the financials do. 9,600+ satellites. 10.3 million subscribers. 164 countries. A timeline that started with the first LEO constellation deployment in 2019 and reached satellite-to-mobile coverage in 2025.

Here is how 2025 splits across the three segments:

Connectivity (Starlink):

▫️ Revenue: $11.4B

▫️ Operating income: $4.4B

▫️ Capex: $4.2B

Space (launch):

▫️ Revenue: $4.1B

▫️ Operating income: -$657M

▫️ Capex: $3.8B

AI (xAI, Grok, X):

▫️ Revenue: $3.2B

▫️ Operating income: -$6.4B

▫️ Capex: $12.7B

Consolidated:

▫️ Revenue: $18.7B

▫️ Operating income: -$2.6B

▫️ Capex: $20.7B

Q1 2026 tells the same story in a single quarter:

▫️ Connectivity (Starlink): $3.257B

▫️ AI (xAI and X): $818M

▫️ Space (launch): $619M

Starlink generated more than four times the revenue of the launch business in one quarter. The segment that started as the means to fund rockets has become the business.

Three stories inside one company. The consolidated loss of $2.6 billion disappears when you separate them. Starlink is highly profitable. Launch reinvests deliberately. AI bleeds at scale.

Starlink Is the Entire Investment Case

Connectivity carried $11.4 billion in revenue, up 49.8% year over year, with $4.4 billion in operating income and $7.2 billion in segment-adjusted EBITDA. Operating income grew 120.4%.

This is the one part of the company that reads like a scaled, profitable business that public-market investors already understand how to price. Strip everything else away and Starlink alone could justify a few hundred billion of the valuation. The remaining trillion-plus is a bet on what the launch and AI segments become.

The AI Segment Dominates the Losses

The losses concentrate in one place. The AI segment lost $6.4 billion from operations in 2025 and consumed $12.7 billion of capex. In Q1 2026 alone, AI capex hit $7.7 billion, an annualized pace above $30 billion.

The consolidated Q1 2026 net loss of $4.3 billion is mostly the xAI burn pulling an otherwise healthy company underwater. The merger turned a profitable launch-and-connectivity company into a heavy loss-maker overnight, by design.

Space Runs at a Loss on Purpose

The launch segment posted a $657 million operating loss in 2025, driven by $3 billion of Starship research and development. Starlink exists because Falcon made launch cheap. Now launch reinvests every dollar into Starship, the vehicle SpaceX needs for V3 satellites, satellite-to-mobile, and eventually orbital data centers.

The operating metrics disclosed in the S-1 show the scale of what this launch infrastructure has already built:

▫️ Roughly 650 total launches completed

▫️ 85%+ of missions flown with reused boosters

▫️ 80%+ of 2025 global mass to orbit carried by SpaceX

▫️ 1GW+ AI compute nameplate draw at COLOSSUS

The economics are deliberate. Each segment funds the next frontier. This is the same playbook Elon laid out in the original SpaceX strategy deck years ago.

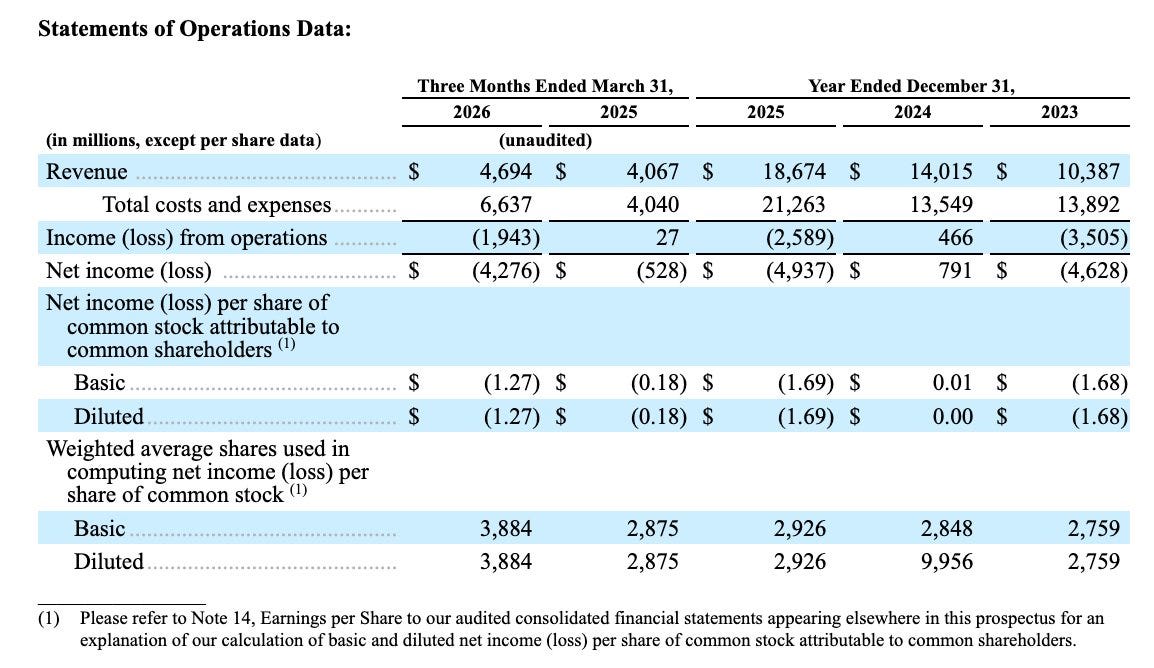

The Actual Financials From the S-1

The income statement tells the story that the segment breakdown abstracts. In 2024, SpaceX was profitable at $791M net income. In 2025, after the xAI merger, the company posted a $4.94 billion net loss. In Q1 2026, a single quarter loss of $4.28 billion.

The merger turned a profitable company into a loss-maker. That is not a red flag. It is a strategic choice. Understanding which one matters enormously for pricing the IPO.

If you want to run the valuation math yourself, the financial models archive has every template you need, from DCF models to exit scenario tools to IRR calculators. The exit scenario model is particularly relevant here.

Starlink’s Quiet Warning Sign

Subscribers more than doubled, from 5.0 million in Q1 2025 to 10.3 million in Q1 2026. Impressive on its own.

Now look at revenue per subscriber:

▫️ 2023 — $99 monthly ARPU

▫️ 2024 — $91 monthly ARPU

▫️ 2025 — $81 monthly ARPU

▫️ Q1 2025 — $86 monthly ARPU

▫️ Q1 2026 — $66 monthly ARPU

ARPU fell 23% year over year. Volume is doing the heavy lifting on revenue growth while per-subscriber economics keep softening as Starlink pushes into lower-priced international and consumer markets. Revenue growth stays strong for now because subscriber adds outrun the price decline. At a 90x-plus revenue multiple, the direction of that per-unit line matters more than the market is currently treating it.

ARPU compression with volume growth is a pattern worth modeling carefully before accepting the headline revenue number at face value. Use the AI-powered stock research prompts to stress-test the subscriber economics before June 12.

The Cash Math Forces This IPO

Cash fell from $24.7 billion to $15.9 billion in a single quarter. Operating cash flow stayed positive at $1.0 billion in Q1, while investing outflows reached $16.7 billion. The company bridged the difference with financing: $7.1 billion raised in the quarter, on top of $29.1 billion of total principal debt and a fresh Bridge Loan signed in March 2026.

At the current AI capex pace, the $75 billion raise reads less like ambition and more like necessity. This is a company that needs public capital to keep building at the speed it has chosen.

For the business and investing frameworks that apply to decisions like this, the AI Corner archive covers everything from how to analyze an S-1 to how to use AI tools for institutional-grade research.

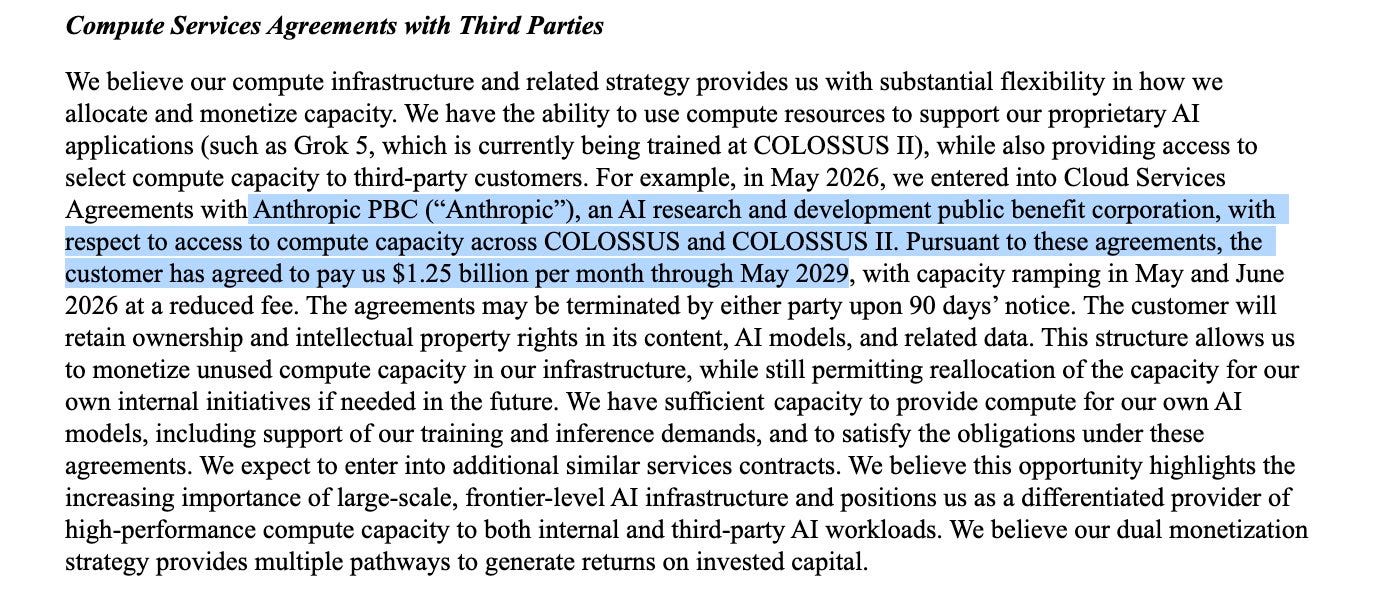

The Deal Buried on Page 13 That AI People Should Read First

Most space coverage skipped this entirely.

In May 2026, SpaceX signed Cloud Services Agreements with Anthropic for access to COLOSSUS and COLOSSUS II compute. The terms: $1.25 billion per month through May 2029, terminable by either party on 90 days notice, with Anthropic retaining ownership of its content, models, and data.

That is roughly $15 billion a year, up to about $45 billion over the term.

Sit with the implication. xAI built the largest coherent AI training cluster on Earth, then started renting capacity to a direct frontier-model competitor. Musk’s compute infrastructure now subsidizes Anthropic’s model training, while xAI trains Grok 5 on the same campus.

For SpaceX, it converts spare compute into one of the largest enterprise contracts in the filing and proves COLOSSUS can sell to the most demanding buyers in AI. It also hands a competitor world-class infrastructure on a short leash. The 90-day termination clause is the tell: this is opportunistic monetization of capacity, reallocatable the moment xAI needs it back.

If you want to understand everything happening at Anthropic and Claude, we cover it in depth. The Karpathy hire this week added another layer: the person leading Anthropic’s pre-training research is now training his models on Musk’s compute cluster.

Musk also invested in DeepMind early on. If you want the full story on Demis Hassabis and the DeepMind MIT deck that predicted the AI era, we broke that down too.

The Cursor Option, Decoded

In April 2026, SpaceX signed a compute and option agreement with Cursor (Anysphere). Two pieces:

Compute agreement. SpaceX supplies GPU capacity and collaborates on models, including Grok.

Option agreement. SpaceX holds the right, with no obligation, to acquire Cursor at a predetermined price. The acquisition, if exercised, would be paid in Class A stock at a $60 billion implied equity value for Cursor. If SpaceX walks, or if Cursor terminates for SpaceX’s material breach, Cursor collects a $1.5 billion termination fee plus an $8.5 billion deferred services fee.

The logic is data. Coding workflows generate high-quality, verifiable, structured signals that improve model training and drive heavy inference demand. SpaceX gets a pipeline of developer interaction data to feed Grok, and a distribution surface inside a high-engagement AI coding tool. The $10 billion combined fee exposure shows how much they value locking that relationship in.

We covered the full backstory on the SpaceX Cursor $60B deal before the S-1 landed.

The $28.5 Trillion TAM, Line by Line

SpaceX calls it “the largest actionable TAM in human history.” Here is what that actually means when you break it down:

The chart tells the story better than any text can.

Space, the business SpaceX is famous for, sits at $370B. Connectivity, the business that actually funds everything today, sits at $1.6T. Then the bars essentially disappear until Enterprise Applications, which towers over everything else at $22.7T.

AI accounts for $26.5T of the $28.5T total. That is 93% of the entire claimed TAM concentrated in a segment that currently loses $6.4B per year.

▫️ Space (space-enabled solutions): $370B

▫️ Connectivity (Starlink broadband and mobile): $1.6T

▫️ AI infrastructure: $2.4T

▫️ AI consumer subscriptions: $760B

▫️ AI digital advertising: $600B

▫️ AI enterprise applications: $22.7T

▫️ Total: $28.5T

The filing itself concedes that several target markets, including in-orbit manufacturing, lunar energy production, and asteroid mining, do not yet exist. The TAM is a vision document wearing a spreadsheet.

What makes the chart worth taking seriously despite the size of the number: Musk has been right about market sizes that nobody believed before. The original SpaceX strategy deck made claims that looked equally detached from reality in 2006. The S-1 is asking you to make the same bet again, twenty years later, at a much higher price.

For the frameworks on how top investors evaluate TAM claims during due diligence, and the pitch decks from companies that made similar market-size arguments before they proved them, the archive has everything. The AI tools and models section also covers how to use Claude to stress-test market size assumptions before committing capital.

The number is almost certainly wrong in absolute terms. The question worth asking is whether it is wrong by an order of magnitude, or wrong the way saying the internet would be worth $1 trillion was wrong in 1995.

The Optionality Stack You Are Actually Buying

Above the Starlink base case, the $1.75 trillion price pays for a stack of unproven bets:

Starship to orbit in 2H 2026. Eleven flight tests done, a twelfth scheduled. Every downstream plan, V3 satellites, V2 mobile, orbital compute, depends on it working on schedule.

Orbital AI compute. Satellite data centers powered by solar, cooled by space, targeted for first deployment as early as 2028. The 100 gigawatt-per-year goal requires moving roughly one million metric tons to orbit annually, which requires thousands of Starship launches per year.

Terafab. A chip-manufacturing initiative with Tesla and Intel, aiming for one terawatt of compute hardware per year. Framework agreement only, with no binding commitment from either partner.

EchoStar spectrum. AWS-4 and H-block licenses, FCC-approved on May 12, 2026, expected to close around November 2027, the key to nationwide satellite-to-mobile coverage.

Each one is a venture bet. Priced together inside a public company at 90x-plus revenue, sold to investors who get one vote per share.

For context on how early-stage venture bets compound into trillion-dollar outcomes, the pitch decks archive shows exactly how companies like SpaceX framed these bets before anyone believed them. The SpaceX strategy pitch deck breakdown is particularly worth reading alongside this S-1.

Governance and What You Actually Hold as a Minority Shareholder

The structure concentrates control completely.

Dual-class shares. Class B carries 10 votes per share. Musk controls 85.1% of combined voting power, owns 12.3% of Class A shares and 93.6% of Class B shares, and will serve as CEO, CTO, and Chairman after the IPO.

Controlled-company exemptions. SpaceX opts out of several Nasdaq governance requirements, including an independent-majority board. Musk can control matters requiring shareholder approval and can elect, remove, or fill Class B director vacancies.

No dividends. SpaceX does not expect to pay Class A dividends in the foreseeable future.

Legal load. The filing flags around $530 million in expected legal costs, active copyright litigation over AI training data, regulatory inquiries into nonconsensual explicit imagery generated by Grok, an Irish DPC GDPR probe, and an FTC inquiry into chatbot safety for minors.

Geopolitical precedent. The 2024 Brazil asset seizure gets its own risk factor, a reminder that a single government can freeze operations over conduct tied to Musk rather than to SpaceX itself.

Government concentration. About one-fifth of 2025 revenue came from US federal agencies, exposing the company to budget cycles and procurement politics.

One structural detail worth flagging specifically for individual investors:

This IPO goes straight to retail. Schwab, Fidelity, Robinhood, SoFi, and ETRADE are all named as selling group members. Retail investors participate at the same initial public offering price as institutions, at the same time. For the largest IPO in history, that is an unusual and deliberate choice.

If you want to use AI to help research and track investments like this, the business and investing tools archive and the AI tools and models guide give you the practical setup. The stock analyst prompts are copy-paste ready.

A Framework for Pricing This

Break the valuation into three layers and decide what you believe at each one.

Layer 1: the Starlink base. A connectivity business doing $11.4 billion, growing roughly 50%, with $7.2 billion of segment EBITDA. This is the part you underwrite with normal tools. Watch the ARPU trend closely. A continued slide below $66 changes the growth story from price-and-volume to volume-only.

Layer 2: the launch platform. Falcon dominates global launch with over 7,400 metric tons to orbit and a 99%-plus mission success rate. Starship turns this into a step-change or a stranded R&D bill. The whole layer hinges on a 2H 2026 milestone.

Layer 3: the AI moonshot. xAI burns $6 billion-plus a year today for the chance to own orbital compute, Grok, and a slice of the largest TAM line in the filing. This is where the trillion-dollar premium lives, and where the financials currently bleed.

The one-liner: you are buying a world-class satellite ISP at a venture multiple, and the premium above it is a bet on Starship, orbital data centers, and Grok, inside a company where Musk holds ten votes for your one.

For investor lists and the databases of funds already positioned in space and AI infrastructure, the VC Corner archive covers who is betting on what. And for the financial models to run your own analysis on the segment economics, every template is there.

Five Things to Watch Between Now and June 12

1. The price range. The first concrete read on whether the market accepts roughly 90x recast revenue or roughly 113x standalone SpaceX.

2. Starship flight twelve. Any slip past 2H 2026 hits the entire growth narrative across every segment.

3. AI segment burn in the pricing amendment. Watch whether Q2 capex accelerates beyond the $7.7 billion Q1 pace.

4. ARPU. A continued slide below $66 shifts the Starlink growth story from price-and-volume to volume-only.

5. The Anthropic contract status. A 90-day-cancellable $15 billion-a-year deal is a swing factor in AI segment revenue. Any change to that relationship between now and June 12 matters considerably.

The largest IPO in history is also one of the hardest to price, because three businesses with opposite financial signatures are being sold as one number. The opportunity and the risk come from the same place: nobody has built this combination before, so nobody has priced it before either.

If you want to track everything happening at the intersection of AI and investing, the AI tools and models and business and investing sections of the AI Corner cover it every week. And the Claude best practices guide is the starting point for using AI to actually do the analysis, not just read about it.

The SpaceX strategy deck breakdown is worth reading again after this teardown. The vision in that deck and the S-1 are the same bet, twenty years apart.

FAQs:

Q: What is SpaceX’s revenue breakdown by segment in the S-1? A: The consolidated 2025 revenue of $18.7 billion combines three segments. Starlink (Connectivity) generated $11.4 billion with $4.4 billion in operating income. The Space (launch) segment generated $4.1 billion with a deliberate $657 million operating loss due to Starship R&D. The AI segment generated $3.2 billion with a $6.4 billion operating loss. Consolidated net loss for 2025 was $4.94 billion versus $791 million net profit in 2024.

Q: What is SpaceX’s $28.5 trillion TAM claim? A: SpaceX describes its total addressable market of $28.5 trillion as the largest actionable TAM in human history. The breakdown: Space at $370B, Connectivity at $1.6T, and AI at $26.5T. AI accounts for 93% of the total, led by enterprise AI applications at $22.7T. Space and connectivity, the businesses generating actual revenue today, represent under 7% of the claimed TAM. The filing concedes several target markets including orbital manufacturing and asteroid mining do not yet exist.

Q: Can retail investors buy SpaceX SPCX shares at the IPO price? A: Yes. The S-1 confirms SpaceX intends to offer shares to retail investors through Charles Schwab, Fidelity Brokerage Services, Robinhood Financial, SoFi Securities, and ETRADE by Morgan Stanley. Retail investors participate at the same initial public offering price as institutional buyers simultaneously.

Q: What is the Anthropic compute deal disclosed in the SpaceX S-1? A: SpaceX signed Cloud Services Agreements with Anthropic in May 2026 for access to COLOSSUS and COLOSSUS II compute infrastructure at $1.25 billion per month through May 2029, roughly $15 billion per year and up to $45 billion over the full term. Either party can terminate on 90 days notice. Anthropic retains ownership of its AI models and data.

Q: How much voting control does Elon Musk have after the SpaceX IPO? A: Musk holds 85.1% of combined voting power through a dual-class share structure where Class B shares carry 10 votes each. He owns 12.3% of Class A shares and 93.6% of Class B shares, and will serve simultaneously as CEO, CTO, and Chairman post-IPO. SpaceX qualifies as a controlled company and opts out of Nasdaq independent board requirements.

Q: Why is SpaceX losing money if Starlink is profitable? A: Starlink generated $4.4 billion in operating income in 2025. The consolidated operating loss of $2.6 billion comes entirely from the xAI segment, which burned $6.4 billion in operating losses on $12.7 billion of capex following SpaceX’s merger with xAI in February 2026. Strip out the AI segment and the launch-plus-connectivity business is profitable. The IPO raises capital primarily to sustain the AI capex burn at scale.

Q: What is the Cursor option agreement in the SpaceX S-1 filing? A: SpaceX signed a compute and option agreement with Cursor (Anysphere) in April 2026. The option gives SpaceX the right to acquire Cursor at a $60 billion implied equity value paid in Class A stock. If SpaceX does not exercise, or if Cursor terminates for material breach, Cursor receives a $1.5 billion termination fee plus an $8.5 billion deferred services fee, totaling $10 billion in downside protection for Cursor.

This money will be used to fund extreme right wing organisations around the world. I’ll keep myself away from these hidden ventures of Elon.

Loved this breakdown. The part I keep coming back to is this piecemeal TAM acting as underwritable revenue.

Just because AI creates $22.7T of economic impact does not mean SpaceX captures that as revenue. The real question is: what percentage can they realistically capture, at what margin, over what timeline, and against whom? Especially on the AI side, the durability question feels huge. How high-margin is that demand once hyperscalers expand capacity, chip supply improves, energy constraints shift, and model efficiency keeps improving? That’s where the valuation feels most aggressive