Airwallex: The Outsider That Built a Billion-Dollar Fintech Empire

Five co-founders. A coffee shop. A rejected $1.2B acquisition offer. And now, a company worth $8 billion.

The $1.2 Billion “No”

When a large company offers a billion dollars to acquire a startup, that’s when almost all founders get the cash and call it quits. That’s when years of uncertainty resolve into a single signature and an exit that few startups ever reach. But this one founder declined.

Stripe once offered to acquire Airwallex for $1.2 billion when the company was generating roughly $2 million in revenue, and Jack Zhang, the CEO, and his co-founders declined.

The decision seemed almost reckless at the time. Building payments infrastructure is expensive, slow, and crowded with competitors that already control large parts of the financial system. Turning down a billion-dollar offer before the business has fully proven itself requires an unusual level of conviction about what the company might become.

Fast forward a decade and Airwallex is now valued around $8 billion and recently crossed $1 billion in annualized revenue while growing close to 90% year over year.

Before we go on:

If you're a pre-seed or seed founder, I got Framer to give this community one full year of Framer Pro free (worth $360)🎁

Used by teams at Perplexity, Midjourney, and hundreds of YC startups. It’s the same tool they use to ship a production-ready site in hours without a dev team, and keep as they scale with CMS, analytics, and AI localization.

If you've been putting off your site or living on a half-baked landing page, now is the time.

In a crowded global payments fintech market, those numbers suggest the founders were solving something larger than a niche payments problem. So what did they see that others didn’t?

Well, the answer might trace back to a small coffee shop in Melbourne, Australia.

Table of Contents

1. A Problem Brewed in a Coffee Shop

2. They Built the Plumbing, Not the App

3. The Numbers Speak Louder Than Words

4. The AI Bet and the IPO He’s Not Ready to Take

5. The Outsider Advantage

6. What Founders Should Actually Take From This

1. A Problem Brewed in a Coffee Shop

Jack Zhang had immigrated alone from Qingdao, China to Melbourne when he was 15 to pursue better opportunities. After studying at the University of Melbourne, he moved through corporate roles in insurance and banking, while simultaneously building side ventures in the shipping and exporting industries.

Zhang was not someone who accepted systems as given. He was an entrepreneur wired into the mechanics of global commerce long before Airwallex existed.

From Frustration to Startup

Now here’s the thing. Every great company begins with a frustration. And for Airwallex, that frustration was literally brewed into existence.

In the early 2010s, Zhang, alongside Max Li, ran a small coffee shop in Melbourne, importing beans from suppliers in China and Brazil. Every time they wired money overseas, they encountered the same infuriating reality. Steep fees, poor exchange rates, multi-day delays, and a system seemingly designed to punish small businesses for operating globally.

Paying overseas suppliers meant sending international wires through the traditional banking system. Each transfer moved through the SWIFT correspondent network, passing between multiple banks before reaching the final destination.

The process was slow, the exchange rates were poor, and the fees accumulated quickly. For large institutions, this friction was manageable. For a small business importing coffee beans, it functioned as a tax on participating in global trade.

That experience sharpened a simple observation. The infrastructure supporting cross-border payments had been designed decades earlier for multinational banks, not for small businesses that suddenly needed to operate globally through e-commerce and digital supply chains.

The Five Co-Founders

Zhang began discussing the problem with a small group of collaborators who would later become the founding team of Airwallex. Max Li, Lucy Liu, Xijing Dai, and Ki-Lok Wong.

Several of them were University of Melbourne alumni, but their backgrounds were notably different. Design, engineering, architecture, and business development all sat around the same table.

That mix of skills shaped an early decision that proved consequential. Instead of building another interface on top of existing payment rails, the team started exploring how to construct their own infrastructure for cross-border payments.

Unlike many fintech startups that rely on existing financial infrastructure, this team was determined to build their own. A decision that would later become their most durable competitive moat.

2. They Built the Plumbing, Not the App

Many fintech companies take one of two paths. They can either build a layer on top of existing banking infrastructure (faster and cheaper), or they invest heavily in building their own global network of licenses, local payment connections, and regulatory relationships (slower, expensive, but defensible).

Airwallex chose the second path.

Instead of routing international transactions through the traditional correspondent banking network, the company began connecting directly to domestic payment systems such as Faster Payments in the U.K., SEPA in Europe, and local clearing networks across Asia.

These connections allow funds to move locally within each market rather than bouncing between intermediary banks through SWIFT.

The result is straightforward but powerful. Cross-border payments become faster, exchange costs fall, and businesses can move money internationally without passing through multiple layers of banking infrastructure.

The pain of building a moat

Perhaps the more significant advantage emerged over time. Airwallex’s infrastructure-first approach required obtaining financial licenses across dozens of jurisdictions, which was a painstaking, slow, expensive process that Zhang and his team navigated over nearly a decade.

But today, that regulatory network is effectively a wall that competitors cannot easily replicate.

And the market has acknowledged this difference. Several large fintech platforms now rely on Airwallex infrastructure to support their own international expansion. Companies such as Brex, Rippling, and Deel use the platform to power global payment capabilities inside their products.

When a competitor becomes a customer, it usually means the underlying system has genuine value.

Jack Zhang summarized the strategy by saying that the company’s real advantage lies in the infrastructure it spent a decade building, both on the regulatory side and within its financial services network.

In practice, that means Airwallex functions less like a typical payments app and more like a fintech infrastructure company that others increasingly depend on.

3. The Numbers Speak Louder Than Words

The most revealing number in the Airwallex story is not the valuation but the pace of revenue growth. The company spent roughly nine years building toward $500 million in annualized revenue.

And then something changed. Within a single year, that number doubled. Airwallex crossed $1 billion in annualized revenue while maintaining growth close to 90% year over year.

That acceleration indicates how the company transitioned from product adoption to infrastructure scale. Once enough companies plug into the platform, revenue begins compounding through multiple financial services at once.

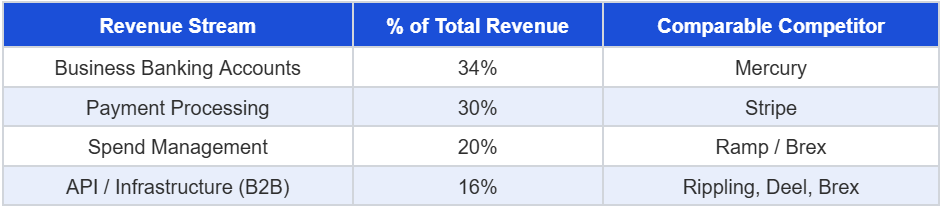

The composition of that revenue tells the real story.

No longer just about payments

The largest segment is business banking for startups, which now accounts for roughly 34% of revenue. In practical terms, this places Airwallex in the same category as platforms like Mercury that provide operating accounts and financial tools for companies.

The difference is that Airwallex built the system with international businesses in mind from the start.

Payments represent about 30% of revenue, placing the company directly in the competitive field occupied by Stripe and other global payments platforms.

Another 20% comes from spend management tools, including corporate cards and expense infrastructure that compete with platforms like Ramp. Companies using Airwallex can issue cards, manage employee spending, and settle payments across borders from the same financial stack.

The final layer is the least visible but increasingly important: infrastructure licensing. Some fintech companies integrate Airwallex directly into their own products, using its payment and settlement network as the underlying engine for international transactions.

At this point, the financial profile of the company reflects this success.

Gross margins exceed 60%, unusually high for a company that moves money across borders. Airwallex reached cash-flow positivity at the end of 2023 and has indicated it expects to reach full profitability again in the fourth quarter of 2025.

In December 2025, investors valued the company at roughly $8 billion, cementing its position as one of the most prominent fintech unicorns of 2025.

Jack Zhang now acknowledges the current competitive landscape with a mixture of humor and candor by saying: “We’re competing with too many people.”

That’s what happens when a financial operating system works. The product surface expands, revenue concentrates, and the company finds itself relevant in categories it didn’t originally set out to own.

And that’s exactly what Airwallex wanted.

4. The AI Bet and the IPO He’s Not Ready to Take

For a billion-dollar startup, the obvious next milestone would normally be an IPO. But Airwallex is not in a hurry.

Jack Zhang has laid out a clear vision for the next chapter of Airwallex’s growth, and it revolves heavily around artificial intelligence.

The IPO trigger: Agentic payments infrastructure

Zhang is developing a wallet product specifically designed to serve as foundational infrastructure for what he calls “global agentic payments.” This is the emerging category in which instead of humans, AI agents will execute financial transactions autonomously.

As AI-driven automation becomes pervasive in business workflows, the question of how AI agents pay suppliers, settle invoices, and manage multi-currency treasury operations becomes a critical infrastructure problem. Zhang wants Airwallex to be the answer.

He defined his IPO trigger as the part where the AI agents business has already scaled to “a few hundred million dollars.”

This is not a company rushing to the exits. It is a company positioning itself for a category that doesn’t fully exist yet.

Stablecoins: Skeptical but watching

Airwallex has hired stablecoin developers and is monitoring the blockchain payments space closely. But Zhang is candid about his skepticism.

Merchant adoption remains very low, and meaningful B2B use cases have yet to materialize. He puts the probability that blockchain meaningfully disrupts global money movement at around 1%, though he notes the team is hedging appropriately given the stakes.

dated June 7, 2025, expressing skepticism about crypto and stablecoins for B2B transactions")

The Road to $10 Billion in Revenue

Zhang has publicly set a goal of reaching at least $10 billion in annual revenue by 2030. He reportedly works around 80 hours per week. From $1 billion to $10 billion in five years, all while building an AI payments layer, expanding into new markets, and navigating an eventual IPO, is an extraordinarily ambitious target.

But for a company that doubled revenue in a single year and turned down a $1.2 billion acquisition offer that now looks like a fraction of its true value, ambition is clearly not in short supply.

5. The Outsider Advantage

The story of Airwallex is, at its core, a story about the power of building from first principles in the face of a problem that incumbents have every incentive to leave unsolved.

The traditional banking system’s inefficiencies in cross-border payments were not bugs. They were features, generating billions in fee revenue for established players.

Jack Zhang and his co-founders saw this not as a reason to accept the system, but as a reason to replace it. And the core strategy begins with geography. The CEO said:

“A lot of the reason we’ve succeeded is we’re an outsider. We’re not part of the Silicon Valley ecosystem.”

That observation is less about culture and more about incentives.

Australia made global thinking mandatory

Most fintech companies built in Silicon Valley start with the same implicit assumption that the United States is large enough to support a meaningful business before international expansion becomes necessary.

You can raise a Series A, find product-market fit, and reach $50 million in revenue without ever seriously dealing with a foreign payment system or a customer who pays in a different currency.

Australia does not offer that luxury. For a startup founded in Melbourne, going global is not a strategic choice made in a board meeting at Series B, but rather the baseline condition for building anything worth building.

That constraint forced Airwallex to design its financial stack around companies that operate across jurisdictions from day one. Not eventually and not as a future roadmap item. There was no domestic version of the product to fall back on.

Necessity, repeated long enough, becomes architecture.

Competing where the giants aren’t looking

Ramp dominates spend management for U.S.-based companies. Stripe built the default for payment processing. Mercury became the go-to for startup banking in the United States.

Each of them excels at its core category, and none of them were primarily designed for the company that needs to pay suppliers in Singapore, collect revenue in pounds, and run expense cards across a team on three continents, all at the same time.

That company existed in growing numbers. It just didn’t have a single platform built around its actual situation. Zhang describes his ideal customer with unusual precision. That is a business selling into Australia, Singapore, the U.K., and Canada simultaneously, needing banking, payments, spend management, and treasury on one platform rather than stitched across five providers.

The value Airwallex offers in that context isn’t just another feature. It’s the removal of a problem those companies had simply learned to live with.

Equally notable is the clarity about where Airwallex doesn’t compete. Zhang has said plainly that if your business operates entirely within the United States, another platform is probably a better fit.

Most companies at this stage avoid that kind of statement because every excluded segment feels like forgone revenue. But knowing who you’re not for tends to be a sign that you’re very clear on who you are.

6. What Founders Should Actually Take From This

The obvious takeaway from Airwallex is the scale of it all. $1 billion in annualized revenue, an $8 billion valuation, and expansion across multiple continents. But those numbers are the outcome, not the lesson.

The more interesting pattern sits underneath the growth curve.

The first is the willingness to build difficult infrastructure before it becomes obviously valuable. For nearly a decade, Airwallex invested in regulatory licenses, local payment connections, and the operational machinery required to support cross-border payments at scale.

That work is slow and expensive, which is exactly why many startups avoid it. Today that groundwork functions as the company’s primary moat. Competitors can replicate features but reproducing years of regulatory and financial infrastructure is far harder.

The second lesson is the advantage of operating from the outside. Because Airwallex did not emerge from the typical Silicon Valley environment, it never assumed that the United States would be its default market. The company had to design for international businesses from day one.

The third pattern is clarity about who the product is not built for. Most startups hesitate to make statements like that because they worry about turning away customers. In practice, clear positioning often sharpens the value proposition for the customers who actually matter.

Which brings the story back to the moment that opened this article.

Turning down a $1.2 billion acquisition offer when revenue was barely above $2 million looked audacious at the time. But it was bold and correct In hindsight, because this kind of clarity only appears after the outcome is visible. The harder moment is earlier, when the numbers are small and the conviction has to come first.

Strong story. Airwallex feels big because it solved a real pain for global businesses, not just made another shiny fintech app. That is what stands out here, real infrastructure pain usually builds the strongest companies.

stripe offered $1.2B when they had $2M in revenue. they said no. now they're at $8B. sometimes the people closest to the problem just know