Stop Asking What Your Startup Is Worth

A VC’s honest take on pricing risk, belief, and hype at the earliest stage.

Having walked into enough pre-seed fundraising conversations, I have started noticing a pattern.

There is a common trait between founders who never succeed at fundraising. They all obsess about their startup’s valuation. And they sometimes end up asking about valuation before even the size of the round is clear. Before the milestones are defined, or sometimes before the product even exists in a form anyone outside the team can use.

And no matter how confident a founder may sound while asking, this specific question almost always hides anxiety, comparison, or worst of all, doubt.

At the earliest stage, valuation feels like a verdict on intelligence, ambition, and credibility. It becomes a proxy for legitimacy. A way to answer the ultimate validation-seeking question:

“Am I being taken seriously yet?”

The problem is not that founders care about valuation, but what valuation is being asked to do at a moment when it cannot possibly deliver certainty.

Before we get into the framework, something worth doing right now:

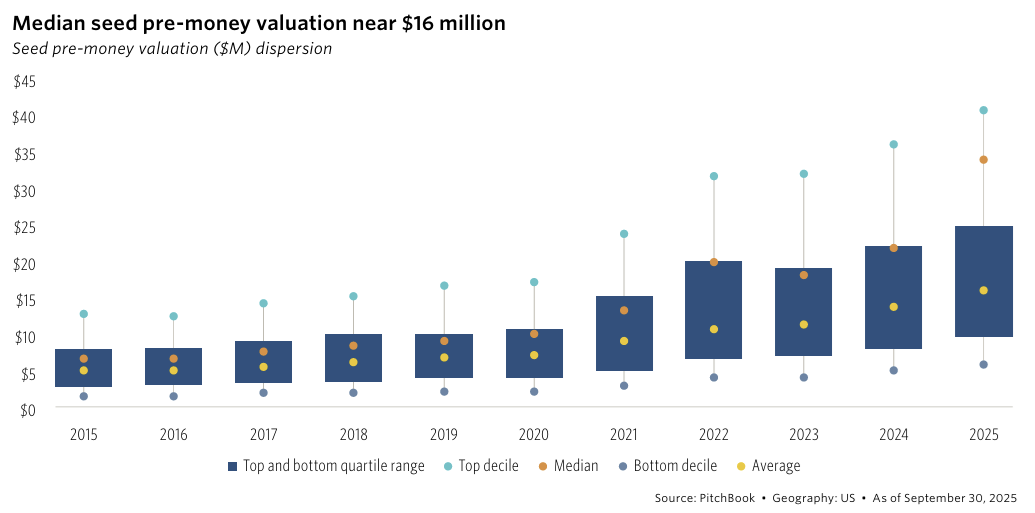

50% of founders raising right now have no clear idea what their company is worth. And investors can tell within the first 5 minutes of a call.

Anchor too high, you kill the deal. Too low, you hand over half your company for free.

The HubSpot Startup Valuation Calculator plugs in your stage, market, and traction and gives you a live estimate built on real market data.

Think of it as a sanity check before you ever sit across from an investor, so you walk in knowing your range instead of guessing at it.

It takes 2 minutes. It is completely free. And it is the conversation you should have with a calculator before you have it with a VC.

Pre-seed valuation is not a truth to be discovered. It is a coordination device, one that tries to align belief, risk, and ownership in a situation where almost everything is still uncertain.

So smart founders need to know how to treat it, how to frame it, and how to use it to secure their fundraising round.

Table of Contents

1. Pre-Seed Valuation Is Not a Measure of Worth

2. Why We Pretend Valuation Is Scientific (And Why That’s Dangerous)

3. What Valuation Actually Encodes at Pre-Seed

4. How the Market Really Prices Pre-Seed Risk

5. Why Everything Breaks When We Treat All Startups Like SaaS

6. Hype Is Not the Enemy. Confusion Is.

7. What Founders and Investors Should Actually Optimize For

8. Valuation Is a Relationship Decision

1. Pre-Seed Valuation Is Not a Measure of Worth

At pre-seed, the word “worth” is basically useless. If you are a founder at the pre-seed stage, you need to remove it from your dictionary.

There is no revenue to anchor against, no stable cash flows, and no product-market fit to validate assumptions. What exists instead is a bundle of unresolved questions.

Can this team execute fast enough? Does the problem remain painful under real usage? Will the market open, or will it resist?

Trying to compress all of that into a single number and call it worth is a category error. Early-stage valuation has nothing to do with accuracy. It’s just an attempt to coordinate under uncertainty.

But if you do put a number on an early-stage startup, then what that number should be doing is balancing three forces that are rarely stated out loud. These usually are:

How much risk the investor is willing to absorb today

How much belief the founder is asking others to share

How ownership should be split so both sides remain committed through the uncomfortable middle

Pre-seed valuations cannot be seen as scorecards. So by keeping the above forces in mind it allows each party to see it as a negotiated truce.

It is not a reward for past progress, but a shared hypothesis about how the future might unfold, with real consequences attached if it does not.

And it should not be seen as a failure of founders or investors. Because early markets are incomplete, information is sparse, and judgment fills the gap.

Before your next investor conversation, use the free valuation calculator to ground your number in real market data rather than intuition. It will not give you the answer, but it will give you the range worth defending.

2. Why We Pretend Valuation Is Scientific (And Why That’s Dangerous)

There is a reason startup valuation discussions reach for formulas even when everyone in the room knows the inputs are fragile. That’s because numbers feel stabilizing and models offer psychological comfort. They provide meaning to uncertainty and make subjective judgment feel objective.

Discounted cash flow models, comparable multiples, and benchmark tables did not appear because they work well at pre-seed. They persist because they make early conversations easier to survive. They give both sides something neutral to point at when conviction is thin and outcomes are unknowable.

In those moments, spreadsheets are less about precision and more about avoiding the discomfort of saying, “This is a judgment call.”

The danger is not that these frameworks exist. The danger is mistaking them for the ultimate truth.

Early-stage valuation frameworks are meant to support judgment, not replace it. When founders optimize for “getting the number right,” they often miss what the number is actually encoding.

This shows up in subtle ways. Founders anchor on a median they saw online and treat it as validation. Investors reference a comparable deal without interrogating whether the underlying risk profile is even remotely similar.

The conversation feels rigorous, but the rigor is cosmetic. Responsibility goes from people to processes.

Over time, this creates downstream damage. Overpriced rounds compress future flexibility. Underpriced rounds will drain ownership and optionality before the company has earned either.

In both cases, the harm does not come from the math, but from outsourcing judgment to something that was never designed to carry it, anno d then pretending the outcome was inevitable.

The HubSpot valuation calculator uses live market data rather than static medians, which means your estimate reflects actual current market conditions rather than a number someone published 18 months ago.

3. What Valuation Actually Encodes at Pre-Seed

A pre-seed valuation compresses a set of assumptions into a single number. It reflects beliefs about how fast progress will happen, how much capital will be required to reach meaningful proof, and how forgiving the market will be if things take longer than planned. It also anticipates future fundability, even when no one names it directly.

What most founders fail to anticipate is how fast those assumptions can harden.

An investor seeks answers from a valuation, and those answers may have to come before the founder manages to articulate them perfectly.

How quickly must this team move? How much narrative polish will be expected by the next round? How much deviation from plan will be tolerated before confidence erodes?

In practice, this shows up in hiring plans that assume velocity that has not yet been proven, or roadmaps that start behaving like commitments instead of hypotheses. What begins as confidence slowly turns into obligation.

A lower valuation doesn’t necessarily mean lack of ambition; sometimes it reflects realism about time, risk, or capital intensity. Sometimes it is a deliberate choice to preserve room for learning before expectations harden. The number itself is less important than the constraints it quietly sets in motion.

Valuation as Future Constraint Pricing

Seen clearly, early-stage valuation is a forecast of future constraints. It prices how much slack the company will have when reality deviates from plan, which it almost always does.

Founders often perceive a higher valuation as freedom. But in reality, it reduces flexibility by eliminating many acceptable future outcomes. A high valuation commits a company early to a narrow set of exits and growth paths, while lower valuations preserve optionality.

This is why two otherwise similar startups can raise at very different valuations and both be rational. The difference doesn’t reflect intrinsic value, it reflects the constraints the founders are choosing to accept.

Understanding where your number sits relative to the market is the first step to making that choice deliberately. The startup valuation calculator gives you that anchor point in 2 minutes. Free, no pitch deck required.

4. How the Market Really Prices Pre-Seed Risk

Founders often approach early-stage valuation as if the market is evaluating the uniqueness of their startup. But that’s not usually the case, as the market is mostly evaluating its own risk tolerance.

Pre-seed valuations cluster because investor behavior clusters. Funds operate under similar return models, similar fund sizes, and similar pressure to stay within what has worked recently.

Angels, in particular, anchor to the last few deals they touched rather than to any abstract notion of intrinsic value.

Geography and timing also play a big part here, even subconsciously, especially in markets where capital circulates through tight networks.

In the U.S., pre-seed valuations have historically settled into narrow bands that expand during optimistic cycles and compress during pullbacks. European markets have traditionally priced lower, not because founders are weaker, but because capital density, exit paths, and risk appetite differ. These ranges track sentiment and structure, not merit.

Benchmarks describe where deals land, not why they work.

Benchmarks Are Guardrails, Not Answers

Benchmarks exist to prevent fantasy, not to confer correctness. They define what is acceptable in a given moment, not what is appropriate for a specific business. That’s why treating medians as validation misses the point.

Underneath those ranges, pricing is shaped by a small set of practical constraints that rarely get stated. There is the amount of capital the company needs to reach its next real inflection, not just survive another quarter.

There is also the level of ownership investors require to justify underwriting that risk at this stage. And there is the psychological limit that founders feel, around how much dilution they can absorb before motivation erodes or future rounds become harder to price.

Change any one of those inputs and the valuation changes completely, even if the business does not.

SAFE Caps and the Myth of Neutrality

SAFEs are often framed as a way to defer valuation. In practice, they relocate valuation into the future under constrained terms. A cap is a belief about where the company should land later, expressed early and without the benefit of clarity.

This becomes consequential when caps accumulate. Each SAFE quietly narrows the range of acceptable outcomes in the priced round. Expectations harden before the company has earned conviction, so what feels flexible at signing becomes pressure at conversion.

This does not make SAFEs dangerous by default, but it makes them consequential. Caps set expectations long before the founder earns clarity, and that destroys any potential flexibility.

5. Why Everything Breaks When We Treat All Startups Like SaaS

Many early-stage valuation heuristics are artifacts of SaaS. That means fast feedback loops, low marginal costs, clear usage signals, and predictable scaling curves.

When these assumptions do exist, early pricing shortcuts are often survivable because reality pushes back quickly. Weak ideas are exposed early, and strong ones will provide the signs you need before capital runs out.

Outside of SaaS, those feedback loops slow down or disappear entirely.

Deep tech, biotech, hardware, and regulated markets operate on different clocks. Capital arrives earlier relative to validation. Time-to-signal stretches, and regulatory drag distorts growth narratives. And thus, applying SaaS-derived valuation logic to these businesses makes no sense, as both risk and patience get mispriced.

In non-SaaS businesses, progress often shows up as de-risking rather than growth. Technical feasibility proven, regulatory milestones cleared, and manufacturing yield stabilized. These are real advances, but they do not map cleanly onto SaaS-style metrics.

When investors expect the wrong signals, founders feel pressure to perform proxies, decks get optimized for optics rather than truth, and narratives drift away from execution. Valuation becomes the pressure point where these mismatches surface, because it is where belief and evidence collide most visibly.

In these settings, valuation mistakes rarely come from choosing the wrong number, but from adopting the wrong clock and organizing the company around it.

6. Hype Is Not the Enemy. Confusion Is.

Every company starts with a bet before the proof shows up. And that’s ok, because that’s how building works. So the problem isn’t hype, it’s when founders can’t explain what would prove them wrong.

If you can articulate what would change your mind, you have a hypothesis. If you can’t, you have a story you’re protecting.

What investors are funding at pre-seed is clarity of thought. The difference between a $5M and $15M valuation often comes down to whether the founder can draw a straight line between what they believe and what they’re testing.

When that line gets blurry, valuation starts compensating for the confusion. Numbers become a substitute for the honest conversation nobody wants to have: What are we actually betting on here, and how will we know if we’re wrong?

7. What Founders and Investors Should Actually Optimize For

If there’s a time when valuation becomes the center of the conversation, something has usually gone wrong.

Founders will obsess about how high the number can go, but what truly matters is the relationship that number could potentially create. The relationship between founder and investor is where the value is.

At pre-seed, valuation is an indication of how uncertainty will be shared when plans collide with reality.

Good early deals rarely feel perfect. They leave both sides slightly uneasy, for different reasons. Founders worry about dilution, whereas investors worry about uncertainty. That tension is healthy because it’s all about the shared exposure to risk rather than one-sided optimism.

Early ownership decisions last longer than founders expect. A survivable cap table preserves motivation, flexibility, and credibility as the company moves into later rounds.

Valuation matters here not because it flatters, but because it decides how much room the company has to learn before pressure sets in.

10 Questions to Expect During a First Call With a VC

The first call with a VC isn’t a pitch competition—and it’s rarely a make-or-break moment.

8. Valuation Is a Relationship Decision

Early-stage valuation is less about uncovering what a startup is worth and more about deciding how uncertainty will be carried forward. How both sides will cope with risk, unexpected events, bumps on the road.

It sets expectations early, prices future constraints, and establishes the emotional contract between founders and investors long before outcomes are visible.

At pre-seed, neither side is purchasing certainty. Founders are inviting others to believe before evidence is complete, while investors are deciding how much ambiguity they are willing to absorb at the outset.

And valuation is the mechanism that aligns those positions when clarity is still distant. It only holds when both sides understand the nature of the commitment they are making, not just the economics attached to it.

Founders who move their focus away from defending a number and toward the kind of relationship that number creates tend to make stronger decisions over time. Those decisions leave room to learn, adapt, and remain credible when progress slows or assumptions break.

The same discipline applies to investors who price risk with restraint rather than performance.

In the end, valuation is not something to be won, it is a commitment that determines behavior long after the round closes and the real work begins.

A high valuation feels great for about five minutes.

Then you realise you’ve just made the next round harder and given yourself less room to get anything wrong.